When the Strait Closes, the World Counts

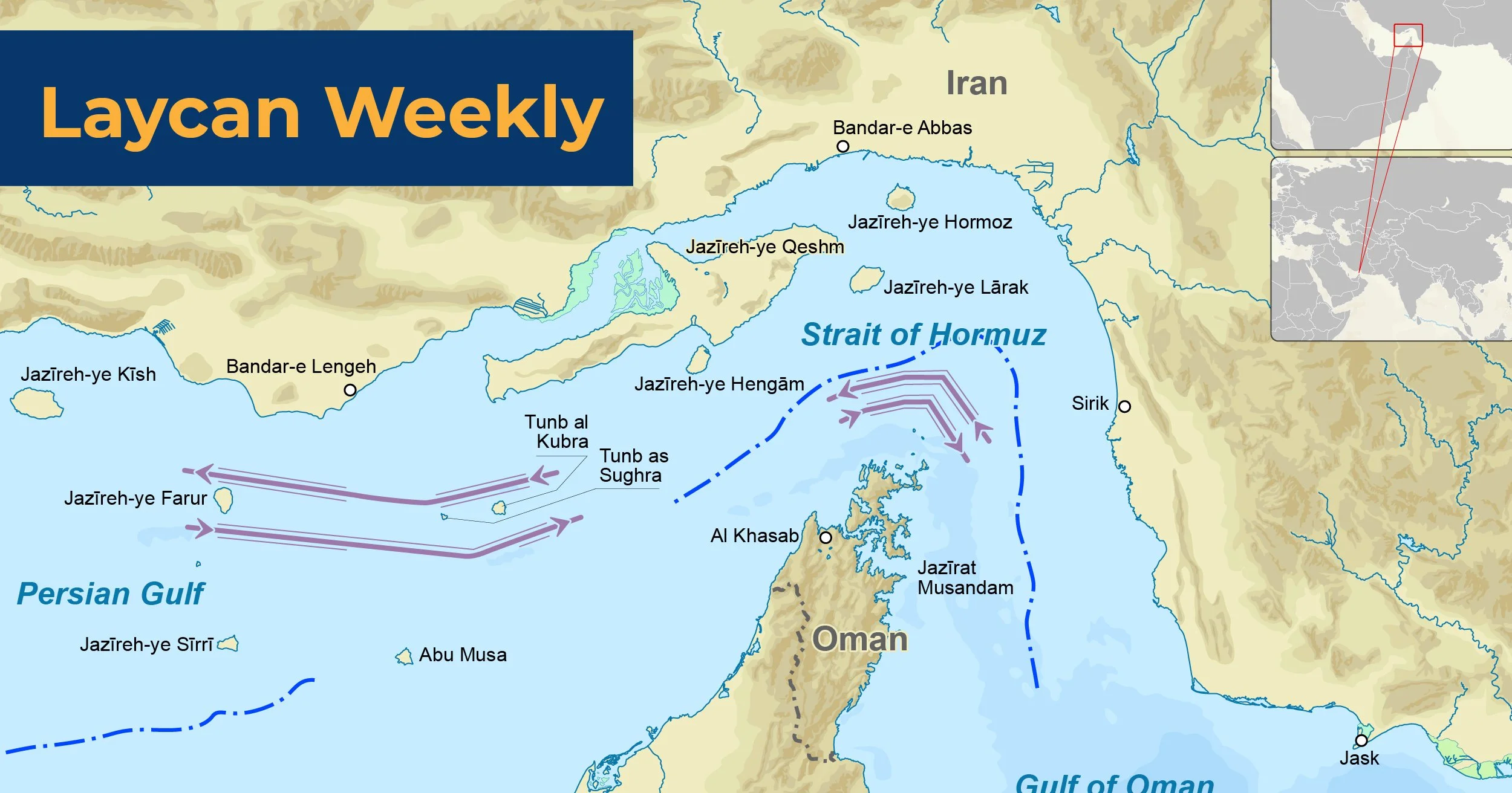

The third week of march, 2026 will be remembered as a hinge point in the modern energy order. The Strait of Hormuz, through which roughly one fifth of the world’s oil and liquefied natural gas has flowed for decades, has been effectively sealed for nineteen consecutive days. Brent crude, which opened 2026 with analysts at the U.S. Energy Information Administration projecting a comfortable annual average of $58 per barrel (www.eia.gov), closed this Friday at $108.23. The International Energy Agency, in an act of institutional urgency without precedent, deployed 400 million barrels from the strategic reserves of its member states on March 11 (www.iea.org). Eight million barrels per day have been removed from global markets, roughly double the disruption caused by the 1973 Arab oil embargo.

The Goldman Sachs scenario matrix (www.goldmansachs.com) now frames three futures: a base case recovery to the seventies by the fourth quarter of 2026 if the Strait reopens gradually from April; a worst case of $111 per barrel by the fourth quarter of 2027 if the closure extends beyond two months; and an extreme risk scenario surpassing the 2008 all-time high of $147 if disruptions prove more durable than any prior crisis. Markets on Friday were pricing somewhere between the first two. The OPEC+ group, which on March 1 agreed to restore 206,000 barrels per day from April (www.opec.org), meets again on April 5 in what may be the most consequential production policy decision in several years.

For Ghana, the consequences are double edged in a way the Bank of Ghana’s own data makes vivid (www.bog.gov.gh). The Cedi has recovered to GHS 10.87 to the dollar, a year-on-year appreciation of nearly thirty percent from GHS 15.53 in March 2025, with February 2026 inflation holding at 3.3 percent according to the Ghana Statistical Service (www.statsghana.gov.gh). The 2026 budget was built on a Brent assumption of $78 per barrel. At $108 and above, the Ministry of Finance (www.mofep.gov.gh) faces a potential petroleum revenue upside of $300 to $400 million beyond the $1.01 billion target. But Ghana imports more than thirty percent of its LPG consumption. With Qatar’s export capacity curtailed by seventeen percent and Hormuz flows disrupted, import costs are rising against the same price environment that is filling the treasury. The National Petroleum Authority’s bi-weekly pricing cycle (www.npa.gov.gh) will not insulate consumers from that arithmetic indefinitely.

Jubilee Field is producing above 70,000 barrels per day, supported by the J-74 well that came online in January 2026 with gross initial production of 13,000 barrels per day, as reported in Tullow Oil’s trading statement (www.tullowoil.com). Tullow’s February 2026 refinancing extended its debt runway to 2028 and 2030. A $225 million government receivable remains unresolved, its settlement now more tractable at elevated prices.

Across the continent, TotalEnergies confirmed a full restart of Mozambique LNG on January 29, the project now forty percent complete and targeting first LNG in 2029 (www.totalenergies.com). On March 20, President Chapo confirmed an ExxonMobil Rovuma FID is expected in the second half of 2026, a thirty billion dollar commitment that would be the largest single energy investment decision in African history (www.exxonmobil.com). The East African Crude Oil Pipeline stands at seventy-nine percent completion, with first oil targeted for July 2026 (www.eacop.com). The world is burning through a fifty-day buffer. African LNG is no longer a choice. It is a requirement.

The three questions that will define next week

Will OPEC+ reverse its April quota increase at the April 5 review and signal a return to production restraint?

Does the Cedi’s GHS 10.87 ceiling hold as LPG and refined product import costs accelerate?

Does ExxonMobil confirm an H2 2026 Rovuma FID, committing thirty billion dollars in the midst of the most severe supply crisis in modern history?

Will OPEC+ reverse its April quota increase at the April 5 review and signal a return to production restraint?

Does the Cedi’s GHS 10.87 ceiling hold as LPG and refined product import costs accelerate?

Does ExxonMobil confirm an H2 2026 Rovuma FID, committing thirty billion dollars in the midst of the most severe supply crisis in modern history?