Africa Focus:A Tale of Continental Parallel Power Plays

Africa’s energy landscape in 2026 is defined by a high-stakes "LNG moment," as the continent transitions from resource accumulation to operational delivery. Across five key theaters, a new architecture of gas strategy is emerging: from the record-breaking "fast-track" floating liquefaction in the Republic of Congo and the steady-state ascent of the Mauritania-Senegal offshore system, to the reawakening of Mozambique’s megaprojects. Meanwhile, Nigeria is pushing toward a 35% capacity expansion with Train 7, and Egypt is deftly pivoting to balance its role as a regional processing hub with new strategic import deals to stabilize domestic demand.

Africa’s LNG Moment: Five Theatres of Gas Strategy

Across Africa, liquefied natural gas developments are accelerating as governments and operators align resource monetisation with energy security, export revenue, and infrastructure expansion. From the rapid deployment of floating liquefaction in the Republic of Congo to Egypt’s evolving import and hub strategy, the emergence of the Mauritania–Senegal offshore system, Nigeria’s expansion of liquefaction capacity, and the restart of Mozambique’s megaprojects, 2025 and 2026 have marked a decisive operational phase for the continent’s gas sector. These developments illustrate a broader shift from reserve accumulation to structured export systems integrated into global LNG trade.

Republic of Congo: The “Fast-Track” Benchmark

The Republic of Congo has emerged as one of Africa’s fastest-moving LNG producers through the Congo LNG development operated by Eni S.p.A.. On December 2, 2025, the company confirmed the arrival of the Nguya floating liquefied natural gas (FLNG) unit and the launch of Phase 2 of the project. The expansion raised the project’s liquefaction capacity to 3 million tonnes per annum (mtpa), marking one of the quickest LNG project deployments recorded in recent years. Construction of the Nguya FLNG unit was completed in approximately 35 months.

Operational progress continued into the following year. On February 7, 2026, the operator confirmed the loading of the first LNG cargo from Phase 2. The milestone demonstrated the operational viability of the project’s modular offshore liquefaction model and positioned Congo LNG as a rapidly scalable export platform.

Investment activity has reinforced the project’s commercial momentum. Commodity trader Vitol secured “Deal of the Year” recognition at African Energy Week 2025 after acquiring a 25% stake in Congo LNG as part of a broader African upstream portfolio expansion that also included the Baleine field offshore Côte d’Ivoire.

The LNG expansion also intersects with domestic energy infrastructure. Gas supplied by Eni fuels the Centrale Électrique du Congo power plant, which accounts for approximately 70% of the country’s electricity generation capacity. Officials within the Ministry of Hydrocarbons have linked the LNG development with the country’s updated Gas Code and national gas master planning framework designed to balance export revenues with domestic energy security.

Egypt: The Strategic Pivot

Egypt’s natural gas strategy entered a new phase on January 4, 2026 when QatarEnergy and the Egyptian Ministry of Petroleum and Mineral Resources signed a memorandum of understanding to supply LNG to Egypt beginning in 2026. The agreement was signed in Doha by Saad Sherida Al-Kaabi, minister of state for energy affairs and president and chief executive officer of QatarEnergy, and Karim Badawi, Egypt’s minister of petroleum and mineral resources.

The agreement reflects structural pressures within Egypt’s gas balance. Domestic production, led primarily by the Zohr field, declined to approximately 4.2–4.8 billion cubic feet per day (bcf/d) in late 2025, while peak summer demand reached about 6.8 bcf/d. This imbalance has pushed Egypt back toward net imports to sustain electricity generation and industrial supply.

Fiscal data illustrates the scale of the adjustment. Egypt’s petroleum import bill for fiscal year 2024–2025 reached US$19.5 billion, an increase of US$6.1 billion compared with the previous year. Natural gas imports accounted for US$3.9 billion of the increase, reflecting the country’s reliance on external supply to stabilise the power system. Oil product imports rose by US$1.7 billion, while crude oil imports increased by US$495.3 million.

Even as imports rise, Egypt continues to maintain its role as a regional gas processing hub. Liquefaction facilities at Damietta and Idku allow the country to process pipeline gas from neighbouring producers and export LNG to global markets. A central pillar of this system is the amended long-term supply agreement linked to the Leviathan offshore gas field.

On August 7, 2025, the Leviathan partners led by Chevron, alongside NewMed Energy and Ratio Energy, signed an amendment to extend gas exports to Egypt through 2040. The revised agreement increases export volumes by 130 billion cubic metres (BCM) and carries an estimated contract value of approximately US$35 billion. Stage 1 of the expanded supply programme, covering an additional 20 BCM, is expected to begin in the first half of 2026 following infrastructure debottlenecking.

The emerging supply framework illustrates Egypt’s dual strategy: securing LNG imports to stabilise domestic consumption while preserving liquefaction capacity for regional and global trade.

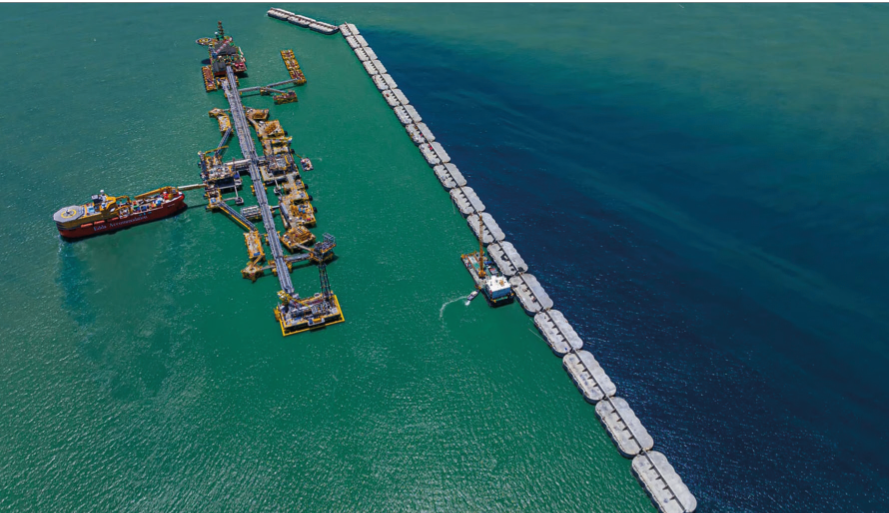

Mauritania and Senegal: The MSGBC Basin Ascent

The offshore gas system shared by Mauritania and Senegal is rapidly establishing the MSGBC basin as a new LNG export province. The centrepiece of this development is the Greater Tortue Ahmeyim project operated by BP in partnership with Kosmos Energy and the national oil companies of both countries.

The project exported its first LNG cargo in April 2025 aboard the LNG carrier British Sponsor. By December 2025, the Gimi floating liquefied natural gas vessel had reached nameplate production capacity of approximately 2.7 mtpa equivalent, with peak output approaching 3.0 mtpa during the month. Production in the first months of 2026 averaged approximately 2.9 mtpa.

The project’s offshore terminal system relies on a specialised engineering design that includes an artificial breakwater constructed from 21 concrete caissons. The structure protects the floating LNG facility and associated infrastructure from Atlantic Ocean conditions, enabling stable offshore liquefaction operations.

The project’s cross-border governance model received recognition at African Energy Week 2025, where the Greater Tortue Ahmeyim development was awarded “Gas Monetization Strategy of the Year.” The award cited the coordinated governance framework established between Senegal’s PETROSEN and Mauritania’s Société Mauritanienne des Hydrocarbures (SMH).

Operational metrics reflect the project’s ramp-up phase. Approximately 18.5 LNG cargoes were lifted during 2025. Project operators expect the number of cargoes to increase substantially during 2026 as production stabilises during the project’s first full year of steady-state operations.

Nigeria: The Push For Train 7

Nigeria is advancing a major expansion of its liquefaction infrastructure through the Train 7 project at the Nigeria LNG Limited (NLNG) complex on Bonny Island. As of early 2026, the project has surpassed 80% overall completion and recorded more than 70 million safe man-hours without a lost-time injury.

Once operational, Train 7 will increase Nigeria’s liquefaction capacity from 22 mtpa to approximately 30 mtpa, representing a 35% expansion of the country’s export capability. The development includes a new liquefaction train and a common liquefaction unit designed to increase throughput across the existing facility.

Construction of the expansion is also generating substantial employment. The project currently supports more than 10,000 workers across direct and indirect roles associated with the Bonny Island construction site.

Policy alignment has accompanied the infrastructure expansion. On January 30, 2026, the federal government, through the Nigerian National Petroleum Company Limited (NNPC Ltd) and the Ministry of Petroleum Resources, launched the Gas Master Plan 2026. The strategy aims to increase domestic gas production to 10 billion cubic feet per day by 2027 and strengthen the country’s capacity to monetise its estimated 210 trillion cubic feet (Tcf) of natural gas reserves.

Mozambique: The Sleeping Giant Awakens

Southern Africa’s largest LNG project resumed activity in early 2026 when operator TotalEnergies announced the full restart of the Mozambique LNG development. The relaunch was confirmed on January 29, 2026 following the lifting of force majeure that had suspended construction activities.

The project restart was announced in Afungi in the presence of Mozambican President Daniel Chapo and TotalEnergies chief executive officer Patrick Pouyanné. Approximately 4,000 workers have been mobilised for the project, including more than 3,000 Mozambican nationals.

Construction of the development is currently about 40% complete. First LNG production is targeted for 2029. Once operational, the project is expected to create approximately 7,000 direct jobs and generate roughly US$4 billion in local procurement and contracting opportunities.

The restart also carries regional implications. Within the Southern African Development Community energy system, Mozambique’s LNG developments are expected to support gas supply to regional markets, including South Africa’s coal-dominated power sector. The project also includes a US$200 million Mozambique LNG Foundation designed to support local development initiatives alongside broader local-content commitments.

Ensemble, these developments illustrate the evolving architecture of Africa’s LNG sector. Some projects emphasise rapid deployment through floating liquefaction, others rely on cross-border governance frameworks or large-scale infrastructure expansion, while several are underpinned by long-term supply diplomacy. Across these five theatres, the continent’s gas sector is increasingly defined by operational projects, structured export corridors, and integrated regional energy systems.